The special tax assessment in case of insufficient manager salary

Click here to find the dutch version of the article.

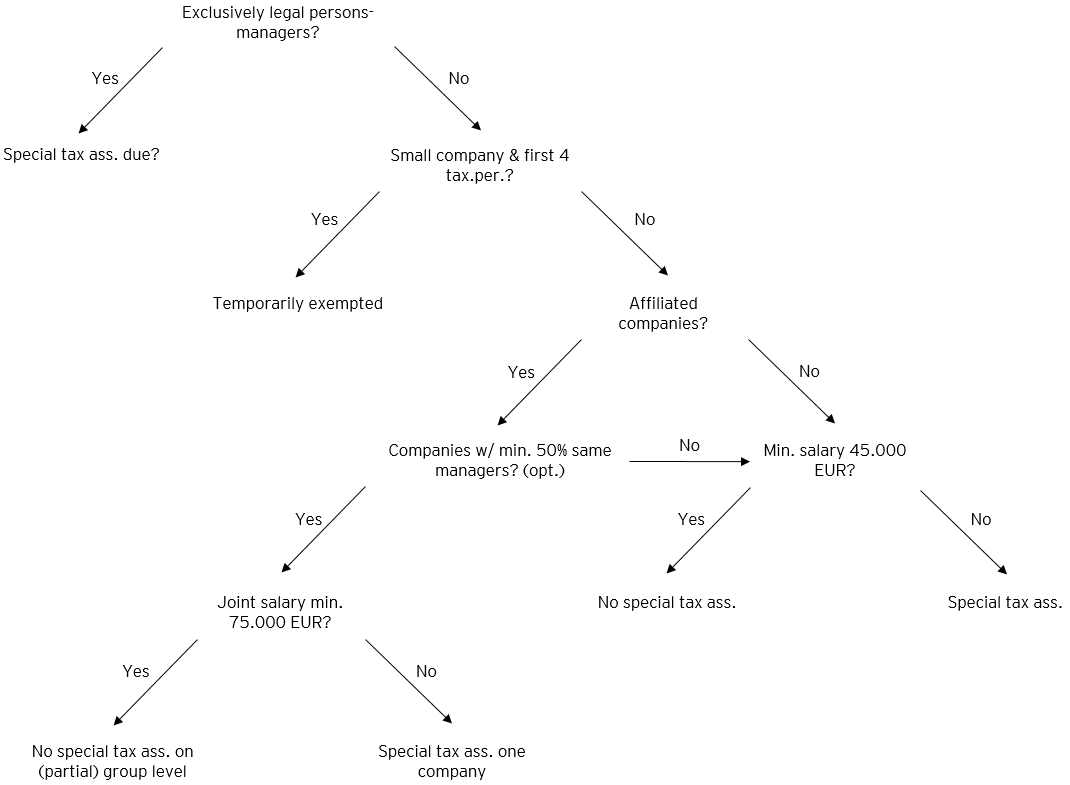

As of 1 January 2018 (assessment year 2019) a new special tax assessment applies in respect of companies who did not pay sufficient management salaries. The rate of the special tax assessment is 5,1% (including supplementary crisis contribution) and would be increased to 10% as of assessment year 2021. This increase, however, would be cancelled by way of repair legislation.

The special tax assessment applies when a company – regardless whether it can apply the reduced corporate income tax rate – did not pay a salary to one of its managers of at least 45.000 EUR. In that case, the taxable base is equal to the positive difference between the aforementioned minimum salary and the highest management salary paid by the company. For related companies, the possibility exists to assess the minimum salary on a global level. In that case the required minimum salary is increased to 75.000 EUR.

This new special tax assessment excels in complexity, in particular with regard to when the special tax assessment applies. Hence, some planning is required in order to avoid the annual cost of 2.295 EUR (including supplementary crisis contribution; as of assessment year 2021 this cost would be increased to 4.500 EUR).

The manager

The special tax assessment can only be due when the company did not pay the minimum salary of 45.000 EUR to one of its managers as mentioned in Article 32 BITC92. This first condition immediately raises important questions for which there are not yet clear answers.

A manager is, by definition, a natural person. What if a company does not have natural persons-managers, for example because it only appointed legal persons as director? It would appear that such companies can never meet the first requirement. In the meantime, the legislator has already taken the initiative to eliminate this uncertainty by way of repair legislation.

Small companies: temporarily exempted

The special tax assessment is not due in respect of small companies pursuant to Article 15, §§1 – 6 Company Code (to be assessed on a consolidated basis) during the first four taxable periods as of its incorporation.

Be aware, the notion “incorporation” has a specific meaning in the context of Article 219quinquies BITC92. If a company’s activity is, in fact, the continuation of an activity previously exercised by a natural person or a legal person, the date of incorporation will be determined based on the first registration in the CBE, respectively the incorporation of the latter.

Affiliated companies

For affiliated companies pursuant to Article 11 Company Code (companies where one company exercises control over the other, companies under central management) of which at least half of the managers in each of these companies are identical, the payment of the minimum salary can be assessed on a global level.

For these companies, the special tax assessment is not applicable when they jointly pay a minimum salary of 75.000 EUR to one of these managers (i.e. a natural person that acts as manager in each of the companies involved).

If these related companies do not jointly pay a minimum salary of 75.000, the special tax assessment will still be due. This tax assessment will then be established in respect of the company with the highest taxable income of the affiliated companies that, each regarded separately, do not pay a minimum salary of 45.000 EUR.

Companies within the same group of whom half of the managers are not the same persons, cannot apply the abovementioned regime. Hence, for each of these companies a separate tax assessment can be established in so far as they did not pay the minimum salary of 45.000 EUR.

Therefore, in order to limit the impact of Article 219quinquies BITC92 in respect of groups of companies, it is important to ensure that at least half of the managers of each of the companies involved are the same persons. In this regard, issues and questions can arise, such as the question whether legal persons-managers and their permanent representatives should be taken into account for the purpose of this calculation. By carefully planning the appointment of managers, the different salaries can be added. Companies each individually paying a salary less than 45.000 EUR will still avoid the special tax assessment when the joint salary for one manager is at least 75.000 EUR.

Schematic overview